How to overcome loss aversion and achieve your financial goals

Is a fear of loss driving your financial decisions? Discover three practical steps you could take to overcome loss aversion and progress towards your financial goals.

Whether you’re playing a board game with family, watching your favourite football team play, or running a race, the chances are that you feel the losses more keenly than the victories.

Indeed, research by the Nobel prize-winning psychologist and economist Daniel Kahneman – who sadly passed away in March 2024 – has shown that we’re hard-wired to feel losses more deeply than gains.

As a result, you might seek out opportunities for avoiding loss rather than focusing on how to make a gain. Kahneman called this “loss aversion”.

Unfortunately, this type of cognitive bias could influence your financial decision making and hamper your progress towards your long-term goals.

Read on to learn more about loss aversion and discover three practical ways to prevent it from negatively affecting your future wealth.

Losses can be felt twice as intensely as the pleasure of gains

According to Kahneman’s Prospect Theory, “losses loom larger than gains”, which leads to loss aversion.

Consider which of these two options you would pick if given the choice:

- A 100% chance of receiving £100

- A 50% chance of receiving £200.

Loss aversion may drive you towards the first option because there’s no risk of a loss – even though you could receive a larger amount by opting for a 50% chance of receiving £200.

Kahneman believed that loss aversion is human nature – we can’t help it. But apply this cognitive bias to your finances, and it might stop you from pursuing growth opportunities that could improve your quality of life.

What’s more, a study by Fidelity (2024) has revealed that this type of cognitive bias may be more prevalent in women. Their data shows that only 27% of women say investing is “for them”, compared to 45% of men.

Loss aversion could lead to limiting financial decisions

Loss aversion could affect your attitude towards saving and investing in several ways.

You might tend to make low-risk choices that limit your returns

The level of return you see on your wealth is often linked to the amount of risk you’re willing to take.

So, an overly cautious approach could potentially make it harder for you to achieve the growth you need to meet your long-term financial goals, such as retiring early or leaving a large inheritance.

For example, as outlined above, a fear of losing money could mean that you shun investing in favour of the seemingly “safe” option of holding your wealth in cash savings.

However, over time, your cash could be gradually eroded in real terms by inflation.

According to the Bank of England’s inflation calculator, to match the purchasing power of a £30,000 cash lump sum put down in 2014, you would need a little more than £40,000 in 2024. This means that in order to keep pace with inflation, your lump sum would have needed to grow by around one-third – an unlikely story if left in a cash account.

In contrast, investing some of your money may have the potential to deliver higher returns over the long term.

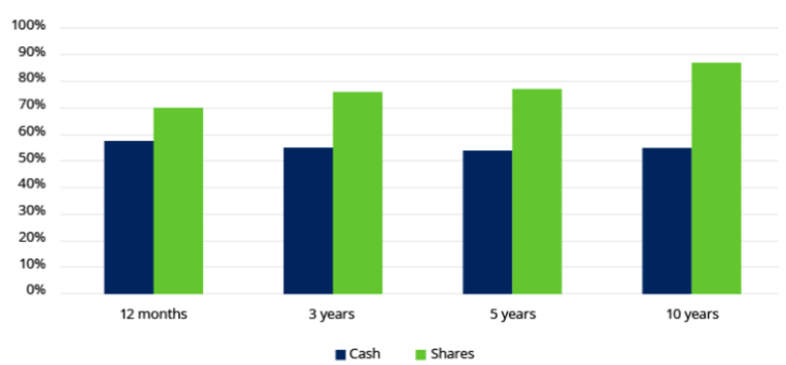

The graph below shows the percentage chance of beating inflation with either cash savings or shares over different time frames.

Source: Schroders (14 March 2024)

So, while keeping some cash as an emergency fund may be sensible, confronting your loss aversion by investing a portion of your wealth over a period of several years could help you achieve your aims more easily.

A fear of loss could lead to emotional decision-making

If you focus too hard on avoiding losses rather than making gains, this could lead to emotional decisions that jeopardise your long-term financial plan.

Imagine that there’s a downturn in the market that negatively affects some of your investments (you might have experienced this if you held investments during the Covid-19 pandemic). Loss aversion could lead you to panic and rush to sell your shares.

As a result, you may miss out on any future potential returns.

Additionally, if you sell your investments as soon as they drop in value, you could make a concrete loss. On the other hand, if you hold on to your shares, the markets are likely to recover and you might make a healthy return.

Indeed, while past performance is no guarantee of future returns, the markets have historically recovered over the long term despite frequent global economic setbacks.

3 practical ways to avoid excessive loss aversion

While loss aversion might be hard-wired in your mind, there are ways you can prevent it from negatively affecting your wealth.

1. Focus on the big picture

Looking at the big picture and focusing on your long-term goals could provide a valuable focus that overrides your instinctive loss aversion.

For instance, if you are tempted to panic-sell shares that dip in value, considering how this might affect your retirement prospects could prevent you from doing so.

Setting clear objectives and building a strategy for achieving them may reduce the risk that you’ll be swayed by short-term fluctuations in the market, temporary changes in your personal circumstances, or investment trends.

2. Make data-driven decisions

Focusing on the numbers and thinking logically could help you avoid making emotional decisions.

However, if you’re naturally risk averse, it might be challenging to keep these emotions in check.

As a financial planner, I can act as an objective sounding board and guide you towards more rational decision-making.

3. Consult a financial planner

By consulting a financial planner, you’ll benefit from the guidance of a trusted expert who can help you combat instinctive loss aversion.

I can help you balance risk effectively and create a financial plan that aligns with your appetite for risk and your long-term goals.

To learn more, just get in touch.

Email lottie@truefinancialdesign.co.uk or call 07824 554288.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.